Uncertainty has been the driving force in 2025 shaped by the complex interplay between economic policy, geopolitical developments, technological investment, and sustainability initiatives on a global scale.

Though the global economy has shown resilience in the aftermath of recent shocks, projected global growth in 2025 was revised downward to 2.8% in the International Monetary Fund’s (IMF) most recent forecast. Geopolitics — including trade tensions, military conflicts and policy uncertainty — weigh on the global economy and increase downside risk. Inflation remains a nuanced issue, with central banks facing the challenge of balancing economic expansion against potential inflationary pressures.

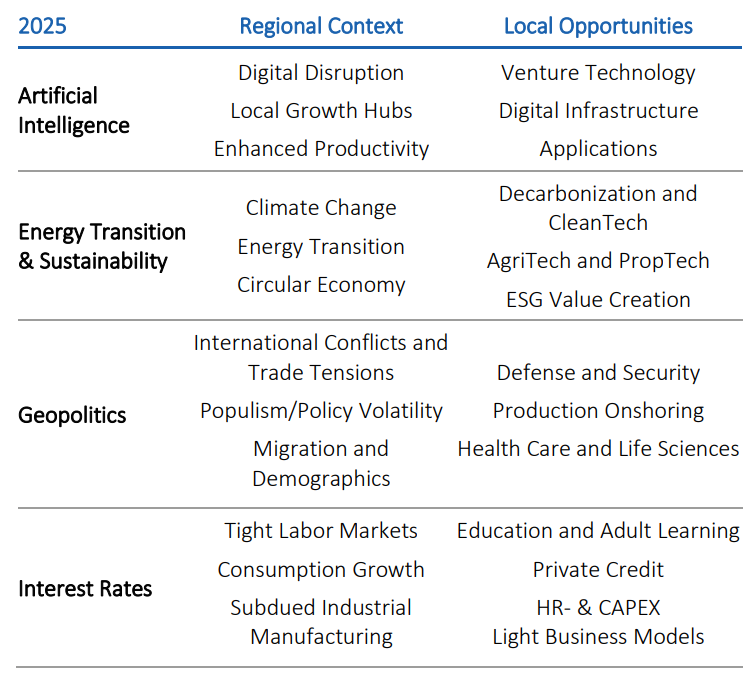

The following megatrends continue to shape the investment landscape for private markets and drive the return opportunity in 2025.

Interest Rates

With inflation moderated from its post-COVID spike, central banks are progressively normalizing policy settings and intend to bring rates back to neutral. While some areas, such as Europe, are cutting rates, other areas, such as the United States, have held rates steady through mid-year. Short-term tariff-driven cost pressures aside, secular inflationary pressures emerging from deglobalization, aging populations, the wealth effect and energy transition may well suggest structurally higher rates going forward. The ripple effects of U.S. geopolitical actions including fiscal policies, immigration policies and tariff applications likely also increase the probability of higher U.S. interest rates over the medium term. While the Mergers & Acquisitions market has appeared to find its footing amongst higher rates, balance sheet pressure remains elevated for the marginal consumer, business and real asset.

Geopolitics

Global geopolitics, shaped by trade tensions, U.S. policies, and broader economic shifts such as deglobalization, are critically influencing the economic landscape in 2025. Strained trade relationships, especially between the United States and China, and the imposition of broad tariffs have created considerable uncertainty with the potential for significant global economic implications. From tail risks in the energy markets to political changes and fiscal debates in countries like France, Germany and Japan that highlight internal challenges and international geoeconomic shifts, much of the geopolitical discussion this year is focused on risk.

Artificial Intelligence

Artificial Intelligence (AI) technology has become a pervasive influence on global markets, with the potential to be a powerful productivity enhancer and disruptor of business models. AI’s use cases in business processes are obvious and plentiful, suggesting a broadening impact beyond the tech sector. The 2025 investment opportunity features not only AI-related hardware and software but also power and digital infrastructure, triggered by the surging resource requirements both upstream and downstream of the data center.

Energy Transition & Sustainability

2025 reflects the ongoing adaptation of global economic structures to incorporate energy transition and sustainability principles, address climate change challenges, and shift toward more sustainable business practices. Although regional disparities exist in energy transition and sustainability priorities, there is broad conviction in the necessity of investment that supports the energy transition, including renewable energy and technology that supports decarbonization.

Regional Context: North America

We find the U.S. economy to be characterized by moderating growth, stable inflation, and monetary easing with policy uncertainty introducing risk to each of these. With this view we have distilled the 2025 global megatrends into regional context and local opportunity themes in the United States.

Source: Wilshire

While U.S. growth, inflation and labor markets remain resilient, the pro-growth posture of the Trump administration is being offset by unprecedented government policy uncertainty. Tariff policy and geopolitical events remain at the forefront, balanced by fiscal measures such as tax cuts and deregulation, and industrial policies focused on re-industrialization and re-shoring that would otherwise boost domestic capital spending. The continuation of policy through acts like the Inflation Reduction Act indicate sustained support for renewables and infrastructure, reinforcing those growth trajectories. The Federal Reserve’s (Fed) focus on maintaining price stability is challenged by the need to balance economic growth with inflation control. Although inflation risk has eased, it remains a complex issue with the potential for fiscal expansions, immigration policy, and tariffs that will exert upward pressure. The tariff impact, in particular, is still unfolding, as it is still unclear how much will be passed through to buyers in terms of higher prices and inflation, and how much will be absorbed by sellers in terms of lower margins and decreased earnings. While U.S. interest rates are expected to continue their decline toward neutral in the second half of 2025, they will likely settle well above post Global Financial Crisis (GFC) levels.

In this period of heightened uncertainty, diversification can be our most effective tool to manage risk. Recognizing that much of the alternatives market is inherently opportunistic, we believe investors should consider positioning their portfolios toward those asset classes that are either uncorrelated or benefit directly from these forces, with managers with the skill to navigate these challenges and capitalize on the complexity that characterizes this current market.

Read Wilshire’s views on private equity, real assets and private credit across North America, Europe and Asia.

CRN: 2025-0801-12764 R

Views expressed are that of Wilshire Advisors. ESG investments are investments made with the intention to generate positive, measurable social and environmental impact in addition to financial return, though outcomes are not guaranteed. ESG investments span multiple asset classes and investment structures. Financial returns can range from the below market to the market rate. Wilshire makes no representation as to the performance metrics of any third-party organizations or the achievement of underlying ESG goals. Where applicable, achievement or compliance with these metrics should be evaluated over the longer-term rather than any shorter time periods indicated.

This material may include estimates, projections, assumptions and other "forward-looking statements." Forward-looking statements represent Wilshire's beliefs as of July 2025 and opinions in respect of potential future events. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual events, performance and financial results to differ materially from any projections. Forward-looking statements speak only as of the date on which they are made and are subject to change without notice. Wilshire undertakes no obligation to update or revise any forward-looking statements.

Wilshire believes that the information obtained from third party sources contained herein is reliable, but has not undertaken to verify such information. Wilshire gives no representations or warranties as to the accuracy of such information, and accepts no responsibility or liability (including for indirect, consequential or incidental damages) for any error, omission or inaccuracy in such information and for results obtained from its use.